Financing

- Home

- Financing

Financing

Are you uncertain about how to finance your upcoming project? We partnered with the best lenders in the industry to offer rates to our clients that no other local custom home builder can match. We can connect you to a select group of lenders who specialize in low-interest rate construction loans and can help you find the best financing option.

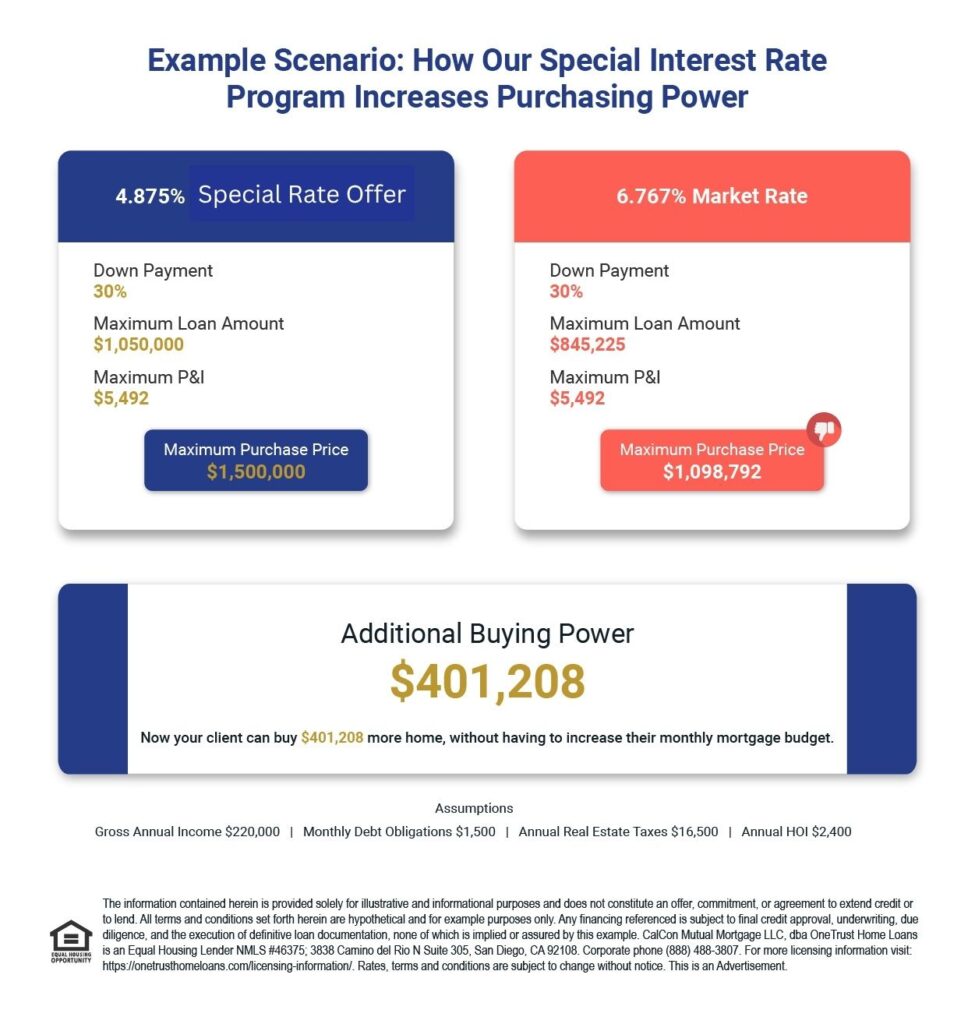

Purchasing Power Difference

Interest Rate 4.875% with 30% down on a $1,500,000 home. Monthly Payment will equal $5,492.

Market Rate 6.767% with 30% down on a $1,098,792 home. Monthly payment will equal $5,492.

Extra Purchasing Power:

$401,208!

*** see below for disclosures for example

What is a construction loan?

A construction loan is a short-term loan used to finance the building of a new home, covering the costs of construction and converting to a permanent mortgage once the home is completed.

How do construction loans work?

What are the costs associated with construction loans?

Construction loans usually come with higher interest rates than standard mortgages and typically require a down payment of 20% to 25% of the total project cost. Borrowers should also budget for closing costs, which can range from 2% to 5% of the loan amount.

Do construction loans have higher interest rates?

Yes, construction loans generally come with higher interest rates than traditional mortgages. This is due to their short-term nature and the increased risk of financing a home that hasn’t been built yet. Rates can vary depending on the lender, your financial profile, and overall market conditions.

If you’re looking to explore current construction loan rates in Washington State, you can check them here.

Contact us today to learn more about financing and our preferred lending experts.

The first step is to get prequalified

To begin the financing process, you’ll submit some basic financial details to one of our trusted lending partners—or work with your own preferred lender. Based on this information, you’ll receive an estimate of how much financing you may qualify for. A dedicated lending expert will guide you through the complexities of construction loans, ensuring you fully understand your options.

Typical Costs of a Construction Loan

The overall cost of a construction loan can vary depending on several key factors, including the size and scope of the project, the property’s location, and the borrower’s financial profile. Because of the added complexity and risk involved, construction loans generally come with higher interest rates and fees than traditional mortgages, but not ours.

Our banking partners offer rates approximately 1.8% lower than the standard rates for resale homes.

In most cases, we are saving you money monthly, while providing you with equity on your new build.

The deposit for your build will cover costs associated with the planning phase of your custom build. These often include the costs of initial drafting, document creation and filing, and design assistance. The initial deposit is currently set at $5000.00, and can be paid by cash, check, wire, ACH, or credit card (additional fees may apply). The initial deposit ensures the drafters are paid for their time invested in the initial drawings of your custom home.

Most construction loans require a down payment ranging from 10% to 30% of the total project cost, but there are programs with as little as 0% down required. This is paid at closing. Our banking partners offer several programs ranging from 0% down VA, 3.5% FHA, Conventional, Jumbo, and many others.

After closing, if you decide to make upgrades or changes to the original construction plans, these modifications often involve additional out-of-pocket expenses. that must be paid for before officially taking ownership of the home.

At Conquest Builders Corp, we work closely with experienced lending professionals to help our clients fully understand these financial requirements. Our goal is to ensure you’re well-prepared—not only for the initial down payment, but also for years of reduced monthly payments and overall cost.

How Loan Disbursements Work

The loan is typically disbursed in a series of payments, or draws, as the construction process progresses. Here’s a breakdown of how a building loan works and the draws at each step:

1. Pre-Construction:

Once we sign an agreement to build for you, there is a deposit of only $5,000.00. After the plans have been finalized and submitted to the bank to schedule our closing, we will submit for the first draw to cover the costs of permitting, final payment to our designers, and initial material orders.

2. Foundation:

The second draw is released after the foundation is poured and inspected, covering foundation and initial site work like excavation or grading.

3. Framing:

Released after framing passes inspection, this draw covers framing, roofing, windows, and doors.

4. Rough Mechanicals:

The third draw is typically released after the rough mechanical systems—such as electrical wiring, plumbing lines, and HVAC installation—are completed and successfully inspected.

5. Insulation and Drywall:

This draw is usually released after insulation and drywall installation is complete and passes inspection. It covers the costs of insulation, drywall, and other related materials.

6. Finish Work:

The fifth draw is typically released after all finish work is completed and inspected. This includes flooring, cabinetry, countertops, painting, and other interior finishes.

7. Final Inspection:

The final draw is disbursed after the final inspection has been completed and the certificate of occupancy has been issued. This draw covers any remaining costs associated with the construction, including cleanup and landscaping.

Looking for land?

***The provided example is a Jumbo Single Close, Construction-to-Permanent Loan Program: This program offers a single loan closing for financing both the construction and permanent phases of your new home. Loan Terms & Repayment: The loan features a 12-month construction phase followed by a 30-year (360-month) jumbo permanent financing phase. Construction Phase (12 Months): Features a fixed interest rate of 7.990% and requires monthly interest-only payments during this period. The initial payment is $3,495.63, based on an assumed initial disbursement of $525,000 (one-half of the total loan amount). Important: The amount of the monthly interest-only payment will increase as additional construction funds are disbursed, up to the full loan amount. The maximum monthly interest-only payment, based on the full $1,050,000 loan amount, would be approximately $6,991.25. Permanent Phase (30 Years / 360 Months): Upon completion of construction, the loan converts to permanent jumbo financing with a fixed interest rate of 4.875% and requires 360 monthly principal and interest payments of $5,556.69. Disclaimer: The stated monthly payment of $5,556.69 does not include amounts for property taxes or homeowner’s insurance. Your actual total monthly housing payment will be higher. Annual Percentage Rate (APR): The Annual Percentage Rate (APR) is 5.200% for this loan, which reflects the total cost of credit over both the construction and permanent phases including interest and financed charges. Down Payment: A minimum 30% down payment is required for this Jumbo loan program. Assumptions & Fees: The rates and payments quoted are based on the following assumptions: a Jumbo purchase loan with a $1,050,000 loan amount, 30% down payment, a minimum FICO score of 720 on a primary residence, and a 60-day rate lock. The disclosed APR of 5.200% is based on the interest rates for both phases and includes $19,765 in Estimated Closing Costs Financed (Paid from your Loan Amount). These financed costs include: $15,750 in Discount Points (1.50% of loan amount), $1,795 Construction Administration Fee, $2,220 Processing Fee and $215 Credit Report Fee. Applicants that are financing land for more than $100,000 require special approval and promotion may vary. The actual interest rate, APR and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by the Lender. Not all applicants will qualify. Rates and terms are effective 7/22/2025 and are subject to change without notice. This offer is available for a limited time only. All options are not available on all programs. There are similar options available with different mortgage types, that require different reduced amounts for down payments. This is an Advertisement. Licensed by the Department of Financial Protection and Innovation under California Residential Mortgage Lending Act, Branch License # 4131248; CalCon Mutual Mortgage LLC, dba OneTrust Home Loans is an EQUAL HOUSING LENDER NMLS #46375; 3838 Camino del Rio N Suite 305, San Diego, CA 92108. Corporate phone (888) 488-3807. For more licensing information visit: https://onetrusthomeloans.com/licensing-information/. | (nmlsconsumeraccess.org)

Mortgage Calculator

Compare Conquest Builders' exclusive rates with current market rates

🏠 Loan Details

⚠️ Important Disclaimer:

The rates and calculations shown are for educational purposes and may not reflect your actual loan terms. Final mortgage rates are subject to credit approval and may vary based on credit score, income, debt-to-income ratio, loan-to-value ratio, and other factors. Not all borrowers will qualify for the advertised rate. Contact Conquest Builders for a personalized quote and to discuss your specific financing options.